North American Lithium

- Second best quarterly safety performance since recommencing operations in 2023.

- Ore mined of 389,801 wet metric tonnes (wmt) was 15% higher quarter on quarter (QoQ).

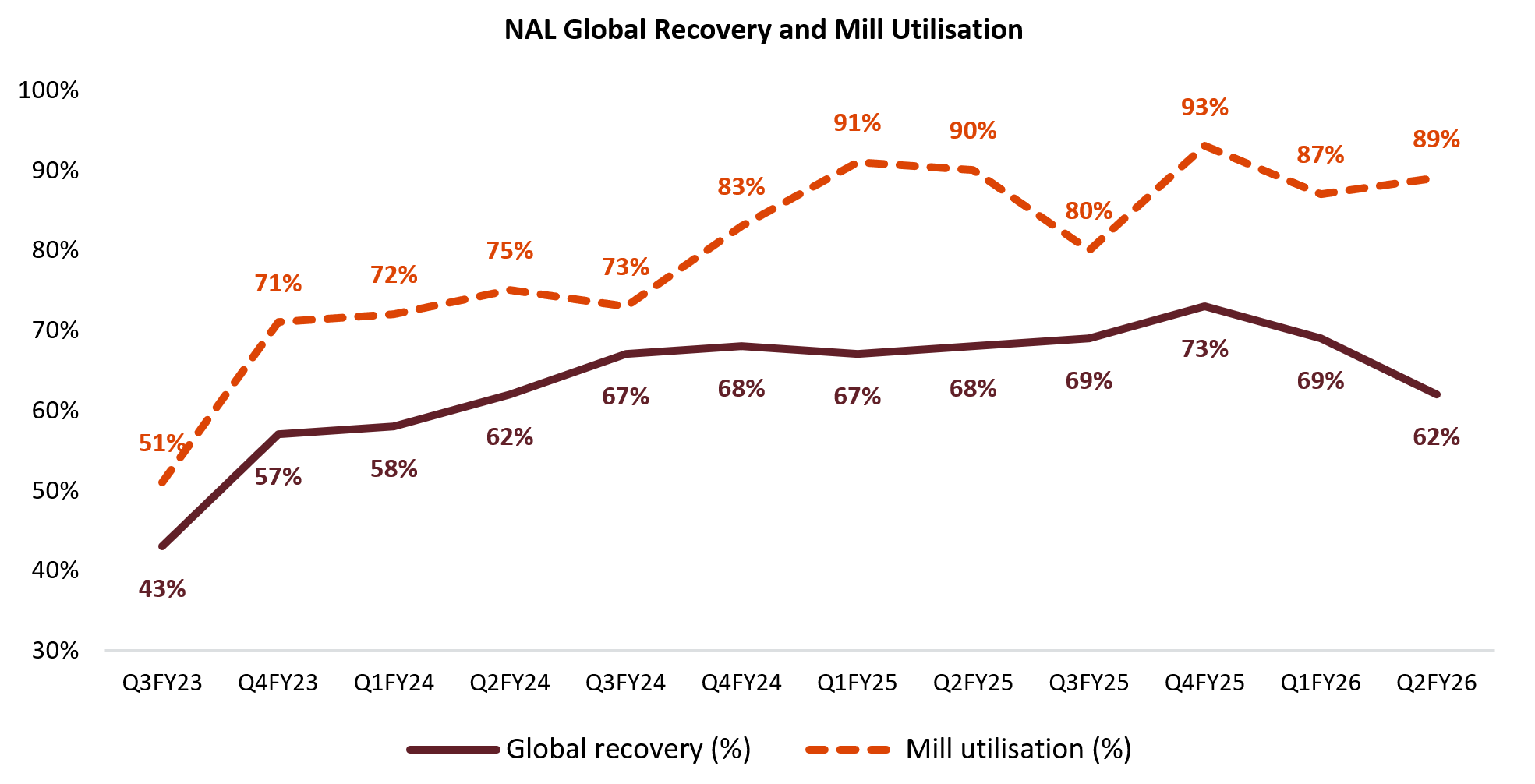

- Process plant utilisation improved to 89%, a 2% increase QoQ.

- Lithium recovery for the quarter was 62%, down 7% QoQ as a consequence of pit development sequencing adjacent to historical underground workings which in turn resulted in temporary lower feed grade and a larger proportion of higher iron content in feed material.

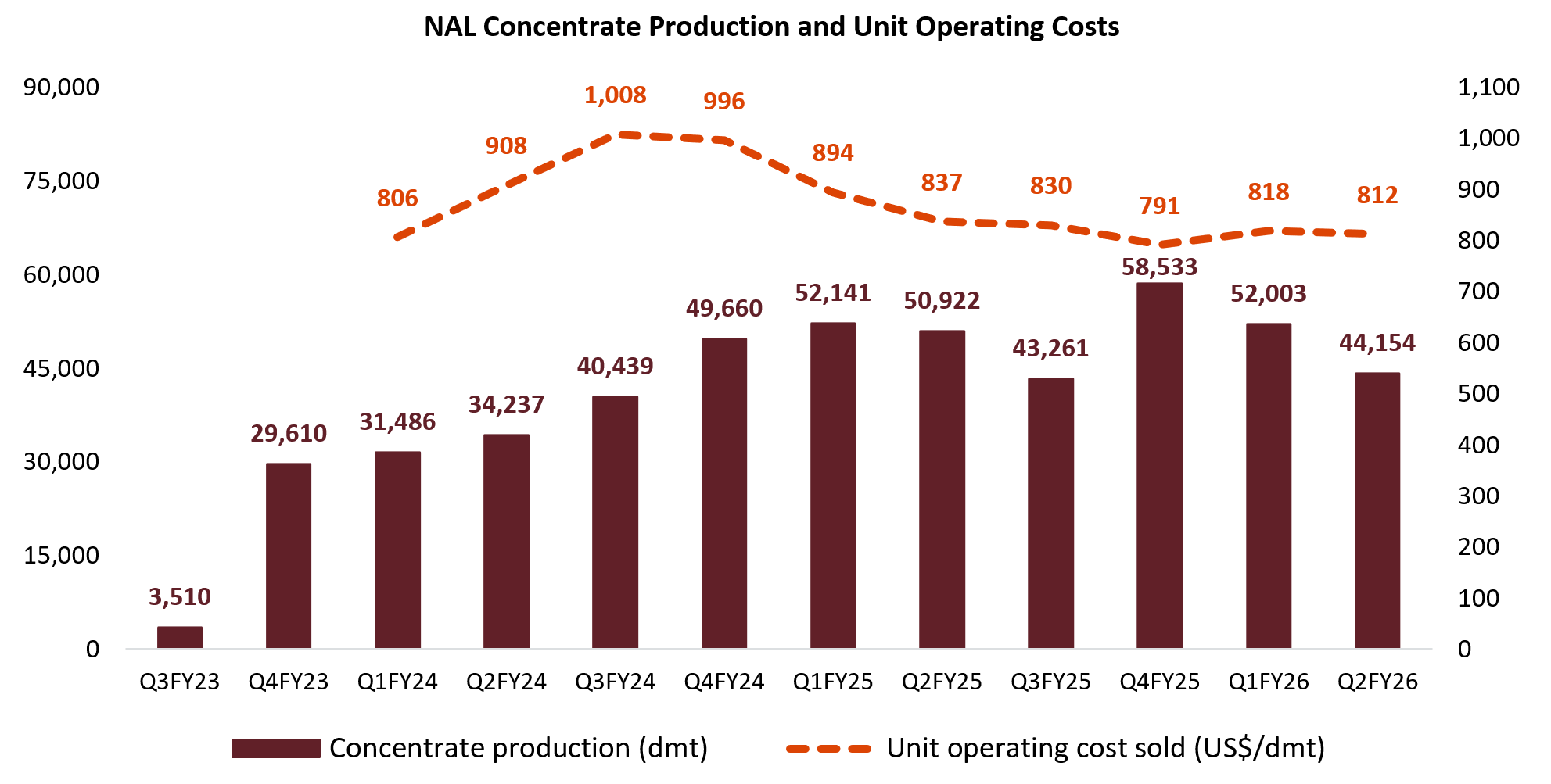

- Spodumene concentrate production declined by 15% to 44,154 dry metric tonnes (dmt) at an average grade of 4.9%. The reduced concentrate production and grade were a function of lower lithium recovery, as the higher iron content necessitated increased use of the WHIMS (wet high intensity magnetic separators).

- Spodumene sales were 66,016 dmt, in line with prior guidance to weight sales toward the

December 2025 quarter1. There were two cargoes sold during theDecember 2025 quarter which aligns with Elevra’s strategy to ship larger cargoes to achieve freight savings. - The average realised selling price (FOB) increased by 27% to

US$998 /dmt versus the prior quarter, reflecting the benefit of improved lithium market fundamentals and Elevra's leverage to rising spot prices. - Unit operating costs (per tonne sold) for NAL were

US$812 /dmt, a modest decrease compared toUS$818 in the prior quarter, resulting in NAL generating a quarterly gross profit for the second time since the restart of operations. - Capital expenditure of

US$7 million for the quarter was on budget and primarily related to the upgrade of the Tailings Storage Facility and other NAL sustaining projects.

Growth Projects

NAL Expansion

- Following completion of the

December 2025 quarter, Elevra issued an update on the NAL Expansion which offered an accelerated timeline to increase annual production and reduce unit operating costs by implementing a phased approach to the expansion2.

Moblan

- Planned baseline environmental field activities were undertaken during the

December 2025 quarter and studies progressed.

Ewoyaa

- Ratification of the Ewoyaa Mining Lease by the

Parliament ofGhana is ongoing. Advancement of the project remains contingent onMining Lease ratification, prevailing market conditions and the availability and structure of suitable project financing.

Carolina Lithium

- During the

December 2025 quarter, Carolina Lithium obtained General Stormwater Permits for the proposed mine and conversion plant advancing key environmental permitting milestones. - In addition, Elevra engaged with local officials, community stakeholders and relevant US government agencies in relation to the next stages of project development, including discussions related to the project’s strategic importance to a US domestic lithium supply chain.

Corporate

- Cash at the

December 2025 quarter end wasUS$81 million , reflecting change-of-control payments and merger-related advisory fees incurred during the period. - Elevra appointed

Christian Cortes as Chief Financial Officer during the quarter, supporting the Company’s operational focus and continued development and growth initiatives. - All resolutions were successfully passed at the Elevra AGM on

21 November 2025 , including election of the four selected ex-Piedmont directors. - Merger related cost synergies remain on track to deliver targeted savings. An update will be provided with the HY26 Interim Results in late

February 2026 . - Elevra has revised FY26 production, sales and cost guidance after reviewing results for the half year - providing a more conservative outlook for the next several quarters. The Company believes it prudent to lower production guidance for the short term until the benefits of increased grade control drilling and improved ore blending are realised. The current operational conditions are not representative of the NAL Life of Mine (LOM) orebody, hence the adjustment applies to near term guidance only.

| Unit | Current Guidance | Prior Guidance3 | ||

| Spodumene concentrate production | Dmt | 180,000 - 190,000 | 195,000 – 210,000 | |

| Spodumene concentrate sales | Dmt | 170,000 - 190,000 | 195,000 – 210,000 | |

| Unit operating cost sold | US$/dmt | US$765– | ||

| Capital expenditures | US$M | |||

Management Commentary

Despite a challenging operating environment at NAL, the Company delivered a significant increase in revenue and positioned the business to capitalise on improving lithium market conditions and future growth at NAL.

The

Operationally, the

Consequently, the Company has revised its production guidance until the benefits of increased grade control drilling and improved ore blending are realised.

Despite these headwinds, unit costs remained broadly consistent with the

Financial performance during the

The increase in revenue highlights the Company’s leverage to improving market conditions and underscores Elevra’s ability to generate meaningful cash flow in a recovering market environment. Despite the short-term operational challenges outlined above, NAL continued to generate operating cash flow during the quarter, underpinned by strong realised pricing, disciplined sales execution and resilient underlying operating performance.

In parallel with our operational focus, the Company continued to advance its development portfolio at Moblan, Ewoyaa and Carolina Lithium. Activities across these projects are progressing at a measured pace to reflect management’s deliberate prioritisation of operational performance at NAL. At Ewoyaa, the Mining Lease continued to progress towards Ghanian Government ratification, while efforts at Moblan and Carolina Lithium remained focused on mid to longer-term project development and positioning the assets within a growing North American lithium supply chain.

Looking forward, management remains encouraged by improving sentiment in the global lithium market and the continued strengthening in lithium pricing. In this context, the Company is advancing plans to increase annual output at NAL at an accelerated rate. We continue to work co-operatively with the

The ability to pursue this growth in a unified and expeditious manner was a primary strategic rationale underpinning the Sayona-Piedmont merger, and management believes the current market environment presents an opportunity to make a meaningful, forward-looking investment into the future of NAL.

With operational and development activities progressing and production guidance appropriately updated, Elevra is well positioned to execute on its growth strategy while maintaining operational discipline and delivering long-term value.

Mr

Managing Director and CEO

Operational Financial Performance

| Unit | Q2 FY26 | Q1 FY26 | QoQ Variance | YTD FY26 | YTD FY25 | YTD Variance | |

| North American Lithium4 | |||||||

| Ore mined | wmt | 389,801 | 338,341 | 15% | 728,142 | 610,683 | 19% |

| Recovery | % | 62 | 69 | (7%) | 66 | 67 | (1%) |

| Concentrate produced | dmt | 44,154 | 52,003 | (15%) | 96,156 | 103,063 | (7%) |

| Concentrate grade produced | % | 4.9 | 5.2 | (0.3%) | 5.0 | 5.3 | (0.3%) |

| Concentrate sold | dmt | 66,016 | 25,975 | 154% | 91,991 | 115,027 | (20%) |

| Average realised selling price (FOB)5 | US$/dmt | 998 | 784 | 27% | 937 | 697 | 35% |

| Revenue | US$M | 66 | 20 | 223% | 86 | 80 | 8% |

| Unit operating cost sold (FOB)6 | US$/dmt | 812 | 818 | (0.7%) | 814 | 861 | (6%) |

| Group | |||||||

| Cash balance | US$M | 81 | 98 | (17%) | 81 | 69 | 17% |

| USD : CAD | $ | 1.394 | 1.377 | 1% | 1.386 | 1.382 | — |

| USD : AUD | $ | 1.523 | 1.528 | — | 1.526 | 1.513 | 1% |

Health and Safety

The Total Recordable Injury Frequency Rate (“TRIFR”) increased during the

The positive trend in safety outcomes is a direct result of strong day-to-day safety discipline across the organisation as teams continue to demonstrate their commitment to proactive and collaborative safety management.

ESG and Community Engagement

Elevra progressed several studies required to support the potential NAL expansion and development of Moblan, and the Company received key permits for future mining and conversion operations at Carolina Lithium. NAL produced an initial self-declaration for Canada’s Towards Sustainable Mining initiative, and the Company is advancing an action plan to achieve Level A certification by the end of CY2027.

During the

North American Lithium

Mining

Ore mined of 389,801 wmt was 15% higher than the previous quarter but at a lower lithium grade of 1.06% delivered to the ROM stockpile.

Mining activity during the quarter focused upon stripping and ore extraction from Phase 3 in order to suitably advance pit development for future mining activities.

Spodumene concentrate production for the quarter was below forecast due to lower than anticipated ore availability around historical underground workings. This resulted in ore being predominantly sourced from volcanic hosted areas of the pit throughout the quarter at a lower lithium grade than anticipated. Whilst volcanic hosted ore typically has higher iron content, the area available for mining over the quarter had an iron content well above the life of mine average. As such the conditions currently being encountered adjacent to historical underground workings are not considered representative of the broader orebody.

These factors combined to materially affect recovery and concentrate production during the quarter.

Grade control drilling density will be increased in the areas of historical underground workings which will enhance scheduling and allow improved ore blending to reduce the impact of high iron ore. Additionally, it is anticipated that mining will progress over the next several quarters out of areas with above average iron content.

Production

Production declined to 44,154 dmt of spodumene concentrate (down 15% QoQ) for the

The mill processed 351,592 tonnes of ore (up 3% QoQ) at an average feed grade of 0.98% Li2O, with some lower grade stockpiled ore complementing ore mined.

Mill utilisation was 89%, a 2% QoQ increase, and broadly consistent with target levels. Mill utilisation was impacted by a planned shutdown to reline the rod mill, while mill throughput for the

The Li2O recovery for the

Increased grade control drilling density, alterations to stockpiling and blending strategies and a continued focus on minimising dilution are actions that will be deployed to manage higher iron pockets coming from the Phase 3 mining area. All of these actions are focussed on improving recoveries whilst we transition through this higher iron area of the mine.

Figure 1: NAL Global Recovery and Mill Utilisation

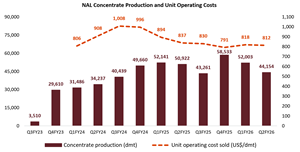

Figure 2: NAL Concentrate Production and Unit Operating Costs (sold)

Sales

NAL revenue was

The increase in revenue resulted from a 154% increase in spodumene concentrate tonnes sold by NAL and a 27% increase in average realised price per tonne (FOB). Total spodumene concentrate sold during the

The average realised selling price (FOB) for the

A total of 29,913 tonnes of spodumene concentrate finished goods was stockpiled at NAL, in transit or at the Port of

Costs

Unit operating costs (FOB) for NAL were slightly lower than the prior quarter at

Total ore mining and waste stripping costs increased 14% QoQ, which coincided with a 15% increase in tonnes of ore mined and 1% increase in waste stripped and mined.

A 3% decrease in ore processing expenditure for the

In-pit and ROM inventory at the end of the

Finished goods inventory decreased as a result of increased shipments and reduced production compared to the

Growth Projects

NAL Brownfield Expansion

Following the release of the NAL Expansion Scoping Study in

The expansion case was submitted to the relevant Federal and Provincial authorities for Environmental and Social Impact Assessment (“ESIA”) determination. Supporting studies progressed, including work in the areas of ecological fieldwork, preliminary geotechnical, hydrogeological and hydrology investigations, and additional hydrogeological testing near the planned expansion area.

Following the conclusion of the

In support of this approach, Elevra plans to update the Scoping Study in early Q2 CY2026 and advance directly to detailed engineering to further de-risk execution and accelerate value creation at NAL.

Moblan

Fieldwork at the Moblan project was undertaken, and an ecological study was finalised while additional studies are expected to be completed in the coming weeks. A project notice to advance, marking the next step in the regulatory and development process, is also planned to complete in the second half of FY2026.

Ewoyaa

Development of Ewoyaa remains subject to ratification of the Mining Lease, prevailing market conditions and attainment of suitable project financing.

Prior to the adjournment of

Carolina Lithium

During the

In parallel, the Company maintained ongoing dialogue with County officials and local community stakeholders to support preparedness for the next stages of development of the Carolina Lithium project. In addition, Elevra continued to engage with relevant US Federal government agencies regarding the strategic importance of the Carolina Lithium project and to explore potential opportunities to increase domestic lithium supply and support broader energy security initiatives.

Elevra has a 49% equity interest in the Morella Lithium Joint Venture, which holds lithium rights in the Pilbara and South Murchison regions. The joint venture is managed by Morella Corporation Limited (ASX: 1MC).

In the Pilbara JV area, a rock chip sampling program of exposed pegmatite outcrops confirmed lithium-caesium-tantalum (LCT)-type pegmatites across the project area. While sampling showed low concentrations of lithium, the results confirmed the presence of rubidium mineralisation and indicated geologic potential for LCT-system development.

At Mt Edon in the South Murchison, hydrometallurgical test work performed by

Elevra holds the lithium and pegmatite rights over the Tabba Tabba project (E45/2364) where exploration is targeting gabbro hosted, flat lying spodumene pegmatite systems. The lease is well located being directly south and along strike from known lithium mineralisation.

In the North drill area a review of drill data has identified a key zone of untested, favourable geology along the western flank of the Corridor Gabbro. At the Pascal pegmatite cluster, 3km along strike to the south, mapping continued to identify untested pegmatite occurrences.

Drilling data collected to date from the North zone and Pascal corridor provide keys to advancing the project and has identified high priority reverse circulation (RC) drill targets. Heritage surveying is planned, following which initial RC drill testing is scheduled for late calendar 2026.

Corporate

Outlook

Updated FY26 Guidance

Elevra has revised FY26 production, sales and cost guidance after reviewing results for the half year providing a more conservative outlook for the next several quarters. The Company believes it prudent to lower production guidance until the benefits of increased grade control drilling and improved ore blending are realised.

| Unit | Current Guidance | Prior Guidance 10 | |

| Spodumene concentrate production | dmt | 180,000 - 190,000 | 195,000 – 210,000 |

| Spodumene concentrate sales | dmt | 170,000 - 190,000 | 195,000 – 210,000 |

| Unit operating cost sold | US$/dmt | ||

| Capital expenditures | US$M | ||

Appointment of

During the

AGM

The first Elevra Lithium Annual General Meeting was held on

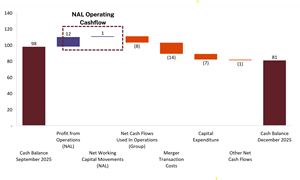

Cash

Cash and cash equivalents decreased by

NAL generated profit from operations of

Outside of NAL, the Group reported a net operating cash outflow of

Elevra paid

Figure 3: Net cash flows for

Merger related cost synergies remain on track to deliver targeted savings. An update will be provided with the HY26 Interim Results in late

Capital Structure

At

- 169,329,111 ordinary fully paid shares;

- 2,723,613 unquoted options expiring on

31 December 2028 ; - 1,760,737 unquoted performance rights (expiring various dates).

Announcement authorised for release by Mr

Information

The following information applies to this report:

- All references to dollars and cents are

United States currency, unless otherwise stated. - Numbers presented may not add up precisely to the totals provided due to rounding.

The following abbreviations may have been used throughout this report: cost, insurance and freight (CIF); dry metric tonne (dmt); earnings before interest and tax (EBIT); earnings before interest, tax, depreciation and amortisation (EBITDA); free on board (FOB); life of mine (LOM); lithium carbonate (Li2CO3); lithium hydroxide (LiOH); lithium oxide (Li2O); net present value (NPV); run of mine (ROM); thousand tonnes (kt); tonnes (t); and wet metric tonne (wmt).

Forward-Looking Statements

This report may contain certain forward-looking statements. Such statements are only predictions, based on certain assumptions and involve known and unknown risks, uncertainties and other factors, many of which are beyond

The information in this report does not take into account the objectives, financial situation or particular needs of any person. Nothing contained in this report constitutes investment, legal, tax or other advice.

The Company confirms that it is not aware of any new information or data that materially affects the information included in the original market announcement and all material assumptions and technical parameters continue to apply and have not materially changed. The Company confirms that the form and context in which the Competent Person's findings are presented have not been materially modified from the original market announcements.

About

Our flagship operation, the North American Lithium (NAL) mine in

Complementing NAL, the

In

Looking ahead, Elevra is focused on strategic downstream partnerships to enable further value-added lithium production, positioning the Company to deliver a secure, sustainable supply of critical minerals to global customers. Together, these assets establish Elevra as a growth-focused supplier supporting the global energy transition.

For more information, please visit us at www.elevra.com.

Appendix

| Unit | Q2 FY25 | Q3 FY25 | Q4 FY25 | Q1 FY26 | Q2 FY26 | |

| Physicals12 | ||||||

| Ore mined | wmt | 370,409 | 322,407 | 361,883 | 338,341 | 389,801 |

| Ore crushed | wmt | 342,752 | 292,962 | 379,353 | 349,698 | 361,485 |

| Ore processed | dmt | 342,855 | 287,782 | 357,290 | 341,780 | 351,592 |

| Concentrate produced | dmt | 50,922 | 43,261 | 58,533 | 52,003 | 44,154 |

| Concentrate sold | dmt | 66,035 | 27,030 | 66,980 | 25,975 | 66,016 |

| Unit Metrics | ||||||

| Average realised selling price (FOB)13 | US$/dmt | 686 | 710 | 682 | 784 | 998 |

| Unit operating cost sold (FOB)14 | US$/dmt | 837 | 830 | 791 | 818 | 812 |

| Production Variables | ||||||

| Mill utilisation | % | 90% | 80% | 93% | 87% | 89% |

| Recovery | % | 68% | 69% | 73% | 69% | 62% |

| Concentrate grade produced | % | 5.3% | 5.2% | 5.2% | 5.2% | 4.9% |

___________________________

1 See ASX release

2 See ASX release

3 As a result of the Company’s transition from reporting in Australian dollars to US dollars, the prior guidance ranges for unit operating cost sold and capital expenditures have been converted using AUD:USD = 0.65.

4 Numbers presented may not add up precisely to the totals provided due to rounding.

5 Average realised selling price is calculated on an accruals basis and reported in US$/dmt sold, FOB Port of

6 Unit operating cost sold is calculated on an accruals basis and includes mining, processing, transport, port charges, site-based general and administration costs and cash based inventory movements, and excludes depreciation and amortization charges, freight and royalties. It is reported in US$/dmt sold, FOB Port of

7 See ASX release

8 See ASX release

9 See ASX release

10 As a result of the Company’s transition from reporting in Australian dollars to US dollars, the prior guidance ranges for unit operating cost sold and capital expenditures have been converted using AUD:USD = 0.65.

11 See ASX release

12 Numbers presented may not add up precisely to the totals provided due to rounding.

13 Average realised selling price is calculated on an accruals basis and reported in US$/dmt sold, FOB Port of

14 Unit operating cost sold is calculated on an accruals basis and includes mining, processing, transport, port charges, site-based general and administration costs and cash based inventory movements, and excludes depreciation and amortisation charges, freight and royalties. It is reported in US$/dmt sold, FOB Port of

Figures accompanying this announcement are available at:

https://www.globenewswire.com/NewsRoom/AttachmentNg/bd2cc0aa-5dad-48a7-86ae-e3da7e825ece

https://www.globenewswire.com/NewsRoom/AttachmentNg/f6f3e3e1-856a-49e8-826a-064fc2a076bd

https://www.globenewswire.com/NewsRoom/AttachmentNg/6b42ca4b-ceea-4f4e-9bed-d4f0007f5d06

For more information, please contact:Andrew Barber Chief Development and Investor Relations OfficerEmail: ir@elevra.comPhone: +61 7 3369 7058

![]()

Figure 1

NAL Global Recovery and Mill Utilisation

Figure 2

NAL Concentrate Production and Unit Operating Costs (sold)

Figure 3